Taxpayer vs. Tax Authority

Is it Worth Challenging the Tax Authority’s Decision?

The topic of whether it is worthwhile to seek judicial review against a tax authority’s decision and whether the courts effectively exercise legal oversight over tax authority procedures and decisions comes up from time to time.

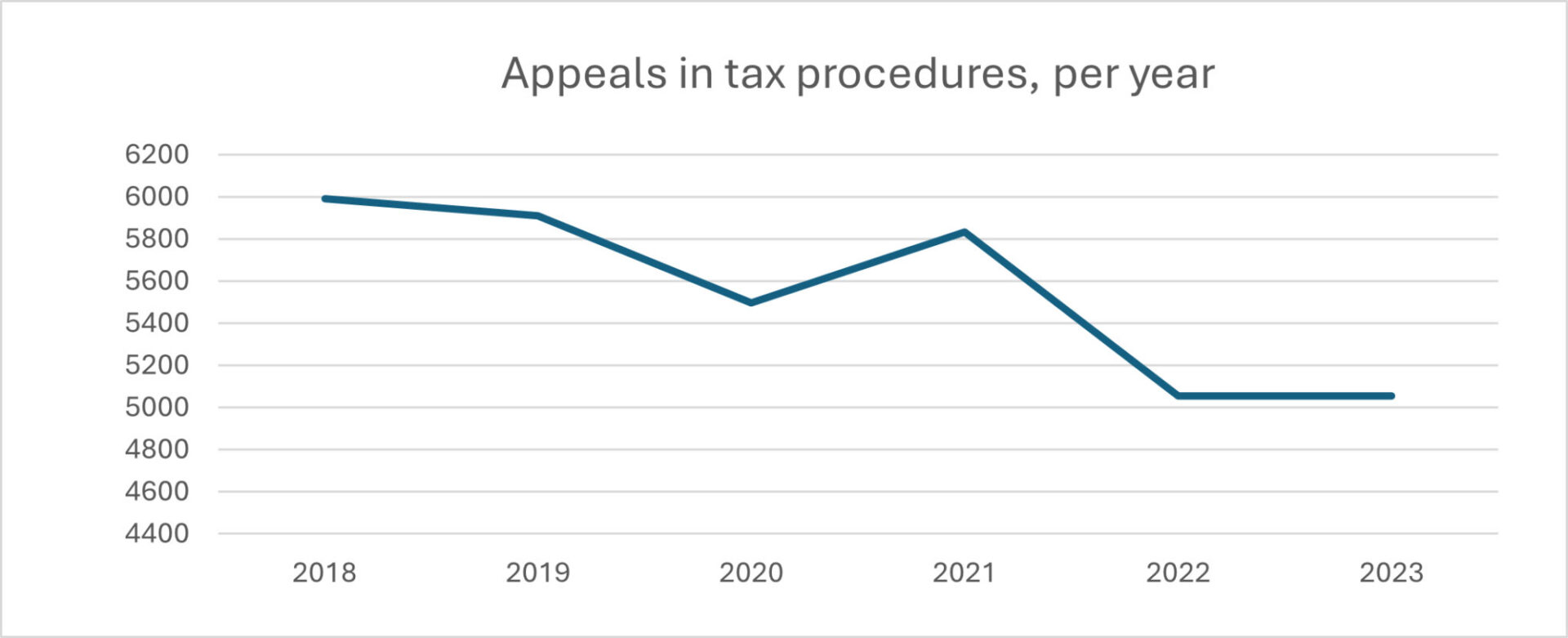

If we look into the numbers of the annual reports of the Hungarian Tax Authority (NAV) and the statistics from the National Judicial Office, we can find some interesting data.

One might attribute this decline to the introduction of the conditional tax penalty mechanism, whose legal basis was established by the legislator in 2018. Under this mechanism, only 50% of the tax penalty is applied to the guilty taxpayer if they accept the first-instance decision and waive the right to appeal against the first instance decision. However, oddly enough, only a small proportion of affected taxpayers, about 10%, took advantage of this opportunity in 2022 (990 cases), while most of the affected taxpayers neither filed an appeal against the first-instance decision nor requested the application of the conditional tax penalty.

Another factor contributing to the decrease in the number of cases could be the increased efficiency provided by the large amount of data collected by the tax authority. Taxpayers realized that the tax authority largely knows the essential data concerning their operations, so tax audits initiated by the authority are typically based on solid grounds, giving appeals less chance of success. This is supported by the large number of e-audits conducted by NAV without the involvement of taxpayers (52,400 cases in 2022).

Appeals Against the Tax Authority’s First Decision

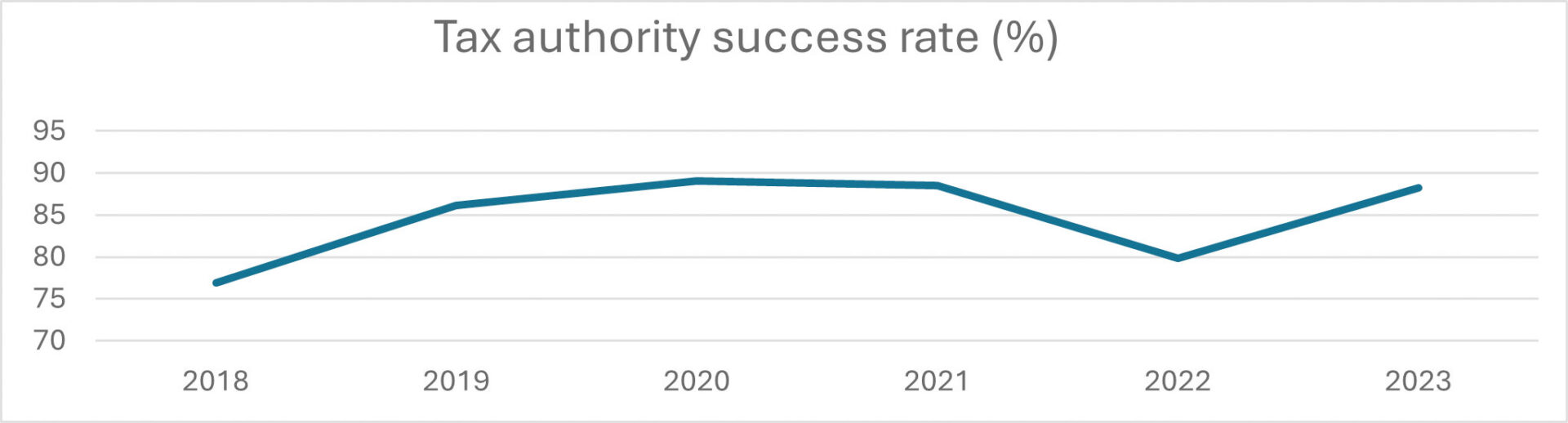

When it comes to the review of appeals, the NAV’s success rate between 2019 and 2023 remained consistently in the 80-90% range: 81.9% – 89.1% – 88.5% – 87.7% – 88.2%. This means that the second-instance tax authority upheld the decision of the local NAV office, which acted at the first instance, in this proportion of cases.

These figures may discourage taxpayers from submitting appeals, as only one out of nine appeals might succeed, while significant money, time, and effort are required to prepare and submit the appeal. However, if we look further at the chances of taxpayers who persist in their belief, a more positive picture emerges.

Judicial Review of Decisions

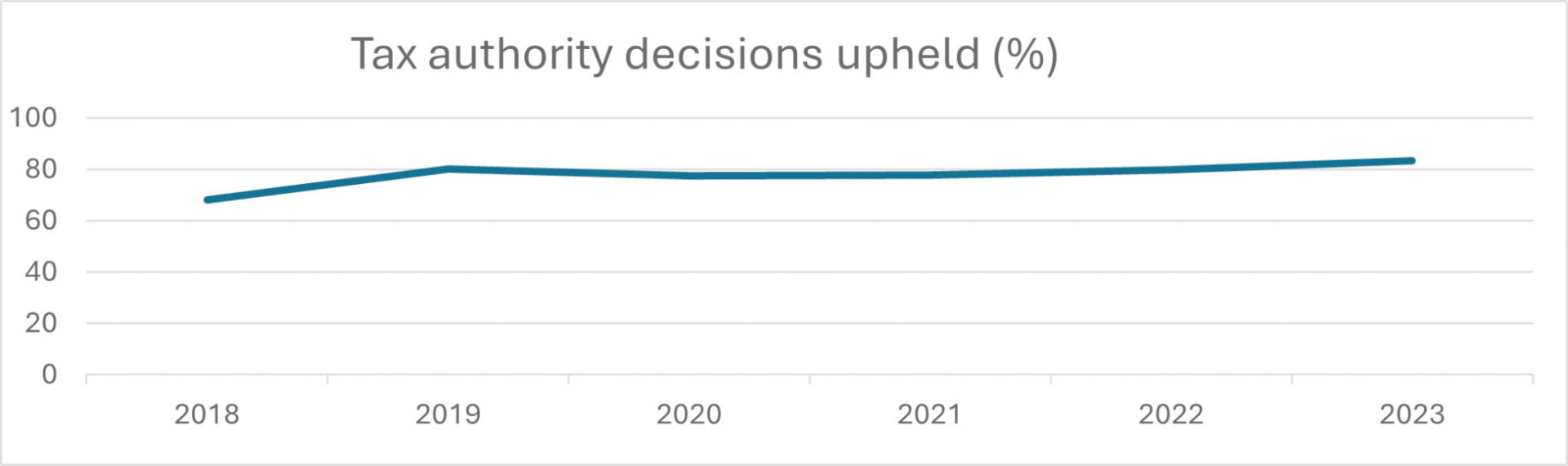

Before examining the success rate of judicial reviews, it is worth noting that, on average, less than one-quarter of final (second-instance) tax authority decisions were challenged in court in 2018, and this number decreased to one-sixth of final cases by 2023. From a professional standpoint, this might seem surprising, as most of the legal work required to prepare and submit the court claim for the annulment of the tax authority decision has been mainly completed during the previous steps (i.e. at the appeal stage), and the losing party only bears the court fees after the judicial review, meaning that taxpayers do not have to advance them.

Once a case reaches the judicial stage, the tax authority’s success rate declines compared to the success of appeals: while in 2018, the NAV won 68.2% of cases in court, this rate varied between 77.6% and 83.3% between 2019 and 2023. Therefore, it can be concluded that it is worthwhile for taxpayers to stand by their position and request judicial review of a decision they find unfavorable, as the court rules in favor of the taxpayer in one out of every four or five cases, according to NAV statistics.

Review Before the Supreme Court – The Curia

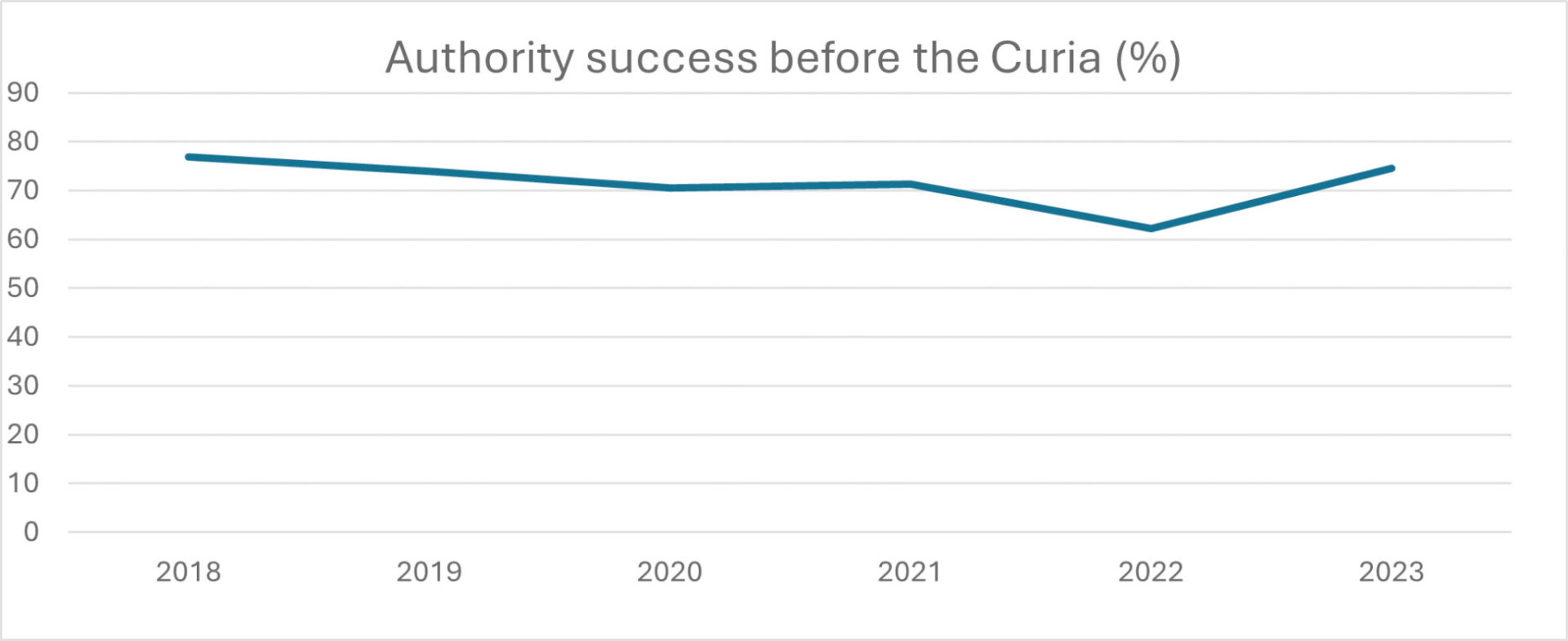

It is clear that, in terms of percentages, Hungarian taxpayers’ efforts to enforce their rights are most successful before the Curia. About 30% of court judgments in tax matters are challenged by taxpayers through a Curia review. Before the highest judicial forum, the tax authority’s success rate fluctuated between 76.9% and 62.2% between 2018 and 2023, meaning that in one-third to one-quarter of cases subject to review, the taxpayer could celebrate at the end of the process.

It is clear that, in terms of percentages, Hungarian taxpayers’ efforts to enforce their rights are most successful before the Curia. About 30% of court judgments in tax matters are challenged by taxpayers through a Curia review. Before the highest judicial forum, the tax authority’s success rate fluctuated between 76.9% and 62.2% between 2018 and 2023, meaning that in one-third to one-quarter of cases subject to review, the taxpayer could celebrate at the end of the process.

Overall, it can be concluded that if a case has reached the judicial stage, it is worth proceeding further and even requesting a Curia review of the court’s decision—provided the legal conditions are met—because the chances of success for taxpayers increase significantly before the next forum.

If you have specific questions or need legal assistance, we are happy to help. Please send us a message or contact us.

This article is for informational purposes only and does not constitute legal advice. Laws and regulations are subject to change, and what is accurate today may not be applicable tomorrow. For personalized advice, please consult with a qualified attorney.

Kapcsolódó bejegyzések

The Hungarian retail tax in 2025: The tax liability of platform operators

The Hungarian Retail Tax in 2025: Tax Liability of Platform Operators The regulation of the Hungarian retail tax entering into force in 2025 has brought significant changes for platform operators. According to the information published by the National Tax and Customs Administration (NAV), operators of online marketplaces and other platforms are no longer merely intermediaries in retail transactions but also bear tax liability. In this article, we provide an overview of…